Thoughts From The Divide: Yield Curves and Friend vs Foe

“Concoct a reason to be concerned”

With inflation stateside and abroad continuing to run rampant (PCE, Spanish PPI, the list goes on…), many recent headlines have centered around the 2-10 spread, which “technically inverted for a few seconds” and “could signal a recession”. Trying to head off any worry, the Fed released a note this week on why such an inversion shouldn’t be feared. Diving into why “the perceived omniscience of the 2-10 spread that pervades market commentary is probably spurious”, the researchers point instead to the value of a metric they call the “near-term forward spread” and assert that any predictive power of inverted spreads is a case of “reverse causality” where the term spreads “have little or no economic impact in and of themselves”. For a counterargument from the Fed itself, see this St. Louis Fed piece, which asked, “Can an Inverted Yield Curve Cause a Recession?” (Cliffs Notes: watch lending)

P.S. As far as central banks go, the current odd man out is the BoJ. Standing its ground for the moment, the BoJ opted for fixed-rate operations to halt rising bond yields and defend its YCC level, though the Yen has been less than happy with the move.

P.P.S. For those looking for some insight into the “Macroeconomic Effects of Asset Purchases” ahead of potential QT, here is an oldie but goodie that finds that, at least early on, “asset purchase programmes had significant positive macroeconomic effects”. Live by the balance sheet, die by the balance sheet?

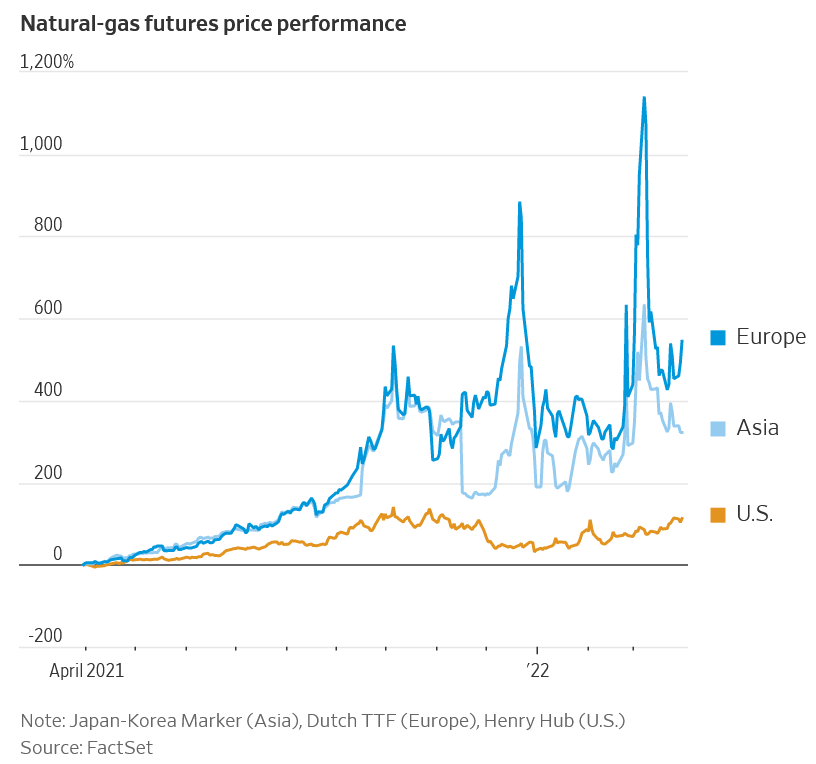

Picking Sides

Continuing on the thread of deglobalization we talked about last week, it’s clear that economic dividing lines are running deeper and becoming more defined. Russia is threatening to force “unfriendly” countries to pay for gas in rubles. Germany is considering expropriating “Gazprom and Rosneft units in the country”, both of which are “systemically important for Germany”. And the US is trying to use a little bit of both the carrot and the stick. On the one hand, it is changing rules and ramping up shipments of natural gas to help the Europeans (at the cost of some price pressure stateside). On the other hand, it is going with the idea that “friends don’t let friends” buy Russian oil at a steep discount and has warned India not to significantly increase purchases nor violate sanctions. Whether the latter tactic yields any dividends remains to be seen, but as economic dividing lines are drawn up, it’s clear that countries are looking for “signs to know faithful friend from flattering foe”.