Thoughts From The Divide – Reap What You Sow

“Not even sure I could get a price today”

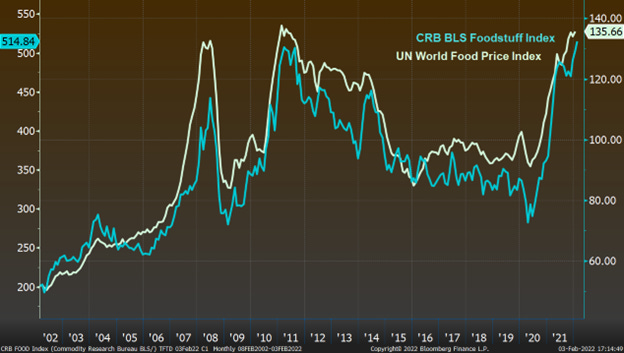

While we can make light of “Let them eat cake” as a meme, food security is no laughing matter, as the 18th century French and 19th century Irish could tell you. While there thankfully aren’t any blights making headlines at the moment, having recovered from both labor and processing issues, the food supply chain is once again facing some turbulence. Building on the bans we discussed here, Russia announced earlier this week that it would no longer be exporting ammonium nitrate fertilizer “from Feb. 2 to April 1” due to internal needs: “Additional demand has arisen on the domestic market for ammonium nitrate from both agricultural producers and industrial businesses”. While perhaps not unexpected as part of the latest saber rattling (fingers crossed it is just that), this move will be felt worldwide, with Russia producing “two thirds of the world’s annual… ammonium nitrate”.

What’s more, tight fertilizer supply and commensurate price increases have had knock-on effects. As one article states, “Escalating costs are leading some farmers to shift acres toward less fertilizer-intensive crops, like soybeans”, while others may opt to skip some planting altogether. As this article notes of global agriculture, rising fertilizer prices are “forcing many to cut back on production” or to look for alternatives, including anecdotal evidence that farmers in Sumatra have “resorted to using monosodium glutamate, or MSG, a flavor enhancer that contains high levels of nitrogen” (See here and here. The more you know!), while others are “trying organic methods, like spreading ash and plant debris on their crops”. Back to the original “pot ash”? But the ripple effects could extend much further. As the WSJ points out, “higher costs for such [farm] commodities would further inflate prices of pantry staples like cereal and cooking oil, as well as beef and other meat because producers rely heavily on grain to feed livestock and poultry”. One step forward, two steps back for “groceries”?

“Inflation could turn out to be higher”

The Bank of England, already ahead of the developed market crowd in raising rates, opted to raise rates 25 bps following its meeting today. The hike resulted from a 5-4 decision in which the minority “had preferred a more substantive hike, to 0.75%”. As justification, the BoE wrote that inflation “is expected to increase further in coming months, to close to 6% in February and March, before peaking at around 7 ¼% in April” (See our comments here on some of the reasons why inflation may already be metaphorically baked in). Bailey cautioned, however, that “it would be a mistake to extrapolate simplistically from what we have done today and assume that rates are now on an inevitable long march upwards”.

The ECB took a different route at its meeting and opted to leave rates unchanged despite record Euro area HICP (similar to CPI) and the latest PPI reading showing prices had increased 26.2% (Yes, 26.2%, not 2.6%, which coincidentally was what HICP hit excluding “energy, food, alcohol & tobacco”). Lagarde did concede that “there was unanimous concern around the table of the Governing Council about inflation numbers” and that risks were “tilted to the upside” but remained steady in her messaging. Regarding the ECB’s actions, she assured markets that the Council would be “gradual in whatever we do” and downplayed, as much as one can a 26% print, by reiterating that “it is energy prices and supply-side constraints that are driving eurozone inflation not excessive demand”.