Thoughts From The Divide – Price Inflation… Now what?

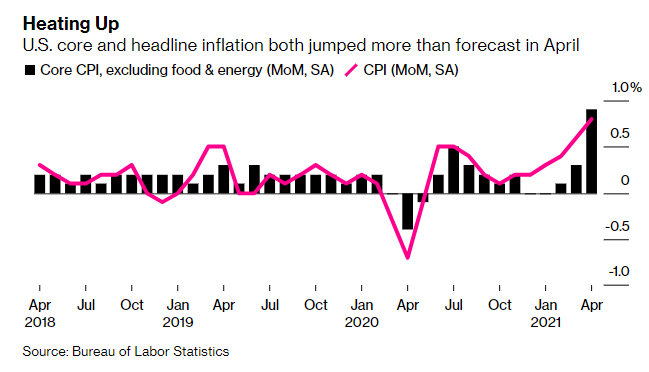

This week’s inflation data blew the doors off of expectations. CPI grew 0.8% MoM and 4.2% YoY, and Core joined the party, rising 3.0% YoY and 0.9% MoM, “its largest monthly increase since April 1982”.Additionally, Producer Prices for final demand goods rose 6.2% YoY, “the largest advance since 12-month data were first calculated in November 2010”, and under the hood, there were some even more impressive jumps. Unprocessed goods for intermediate demand “surged 57.6 percent, the largest rise since jumping 59.3 percent for the 12 months ended August 1973”!

“My concerns… have grown substantially”

Following these data, Larry Summers continued his warnings about inflation in an interview with Bloomberg. Noting that “whether you look at average hourly earnings, whether you look at producer prices, whether you look at consumer prices, whether you look at direct measures of labor shortage, whether you look at market expectations of inflation, whether you look at survey expectations of inflation” “it’s all moved much faster, much sooner than I had predicted, and I think that has to make us nervous going forward”. Additionally, pushing back against the idea that price increases are localized and not “a larger phenomenon”, Summers pointed out that the monthly change in Core CPI equated to double digit growth on a yearly basis. This means that there’s “plenty of room for there to be a lot of transitory factor in it and for us still to have what would be an extremely serious problem”. “I don’t think you can dismiss these figures”. However, Summers admitted that, regarding the idea that this CPI print is a short one off, that “anything is possible and they[, the Fed,] could be right”.

“Do we try to shift lanes?”

Summers is not alone in urging the Fed to think about thinking about thinking about other possibilities. Even before this week’s CPI prints, Stan Druckenmiller and a colleague from Duquesne argued that the Fed was being shortsighted and seemed to be “fighting the last battle”. Their op-ed, “The Fed Is Playing With Fire”, warns that the Fed’s policy “has enabled financial-market excesses” and claims that “keeping emergency settings [on accommodation] after the emergency has passed carries bigger risks for the Fed than missing its inflation target by a few decimal points”. Mohamed El-Erian also makes an argument for the Fed to consider its current course of action. In his op-ed, El-Erian contends that, though it could not know before the pandemic, in moving policy “from preemptive to reactive”, “the Fed may now well be operating under a framework that is more suited for the pre-pandemic world”, leaving themselves open to “a possible policy mistake in the making”.