Thoughts From The Divide – On Deck

“The policy response to the pandemic and its aftermath could have persistent effects”

Ah, the end of summer, when a young central banker’s fancy turns to thoughts of… Wyoming. That is, of course, the Kansas City Fed’s Jackson Hole conference, and this week, all eyes are on Jerome Powell’s speech tomorrow morning (the full agenda will be released later this evening). Ahead of Powell’s speech, a few former and current Fed heads are playing a game of “the Fed loves me, he loves me not, he loves me…”. Meanwhile, as we wait impatiently to hear Mr. Powell’s comments on “Structural Shifts in the Global Economy”, we couldn’t help reminiscing about some past Jackson Hole nuggets. There really is gold in “them thar hills”.

Last year, the inimitable Mr. Kashkari gave a thumbs up to a “1,000-point market rout”, saying, “People now understand the seriousness of our commitment to getting inflation back down to 2%”. The previous year was understandably different, with Powell stating reasons why he believed “elevated [inflation] readings are likely to prove temporary”. In retrospect, many of us wish we had asked what he meant by transitory. It is also worth noting that one of our favorite Fed papers, “Housing Is the Business Cycle”, was first released at Jackson Hole.

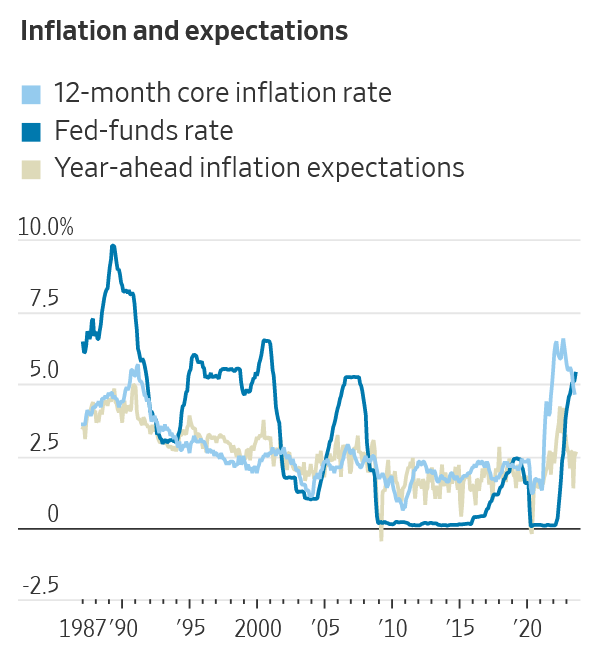

This year, beyond just the question of whether the Fed loves us (and won’t hike rates too much more?), we do have some ideas on what the Fed is thinking about. First is the question of fiscal dominance, which the St. Louis Fed released some research on a few weeks ago. In addition to pointing out that “continuing projected deficits… will eventually lead to a fiscal dominance problem”, that paper mentions that “a significant rise in long-run real interest rates also seems quite possible” with the added warning that “if the bond market does not anticipate a fiscal dominance shock sufficiently far in advance…, then bond investors would be caught with losses on high duration bonds. All of these changes imply that the effects on banks and mutual funds and pension funds and others would be potentially quite dramatic”. Second, we have the latest reporting from “Nickileaks”, including warnings that “with inflation now falling but activity still firm”, the Fed may need to opt “for higher short-term interest rates, or delay interest-rate cuts as inflation falls”. Timiraos reminds us that the Fed could simply stick to an “opportunistic” plan and [try] to get to 2% “gradually over several years by holding rates at a level that could seem slightly higher than they need to be, and letting opportunities, such as the occasional economic slowdown, nudge inflation down bit by bit”. But that has not stopped the ongoing (and possibly unhelpful skirmishing) about whether the Fed should opt to shift its inflation target a little higher to reflect the difficult times we now live in. The latest (un)helpful suggestion came from Jason Furman (following on similar comments from M. Blanchard). Mr. Furman seemed oblivious to the way his comments might be interpreted by bond markets, but perhaps we should think of this as a job application to a future Democrat administration. Reassuring, indeed.

Interested in more MI2?

Our clients tell us that our research allows them to develop a clear, big-picture framework of market conditions, resulting movements, and, most importantly, how to position their portfolios.

We use a series of proprietary, predictive models to anchor our views and create the basis for a repetitive process.

Click here to request a trial and get six weeks of FREE access to our Institutional Research to see for yourself.