Thoughts From The Divide – Fed Maybe, Energy Encore, and Definition Games

“I would certainly say it’s an uncertain thing”

This week saw another Fed meeting and, as has been the case recently, another hike. This week’s 75 basis point hike was not a surprise after earlier inflation readings and the talking back of a potential 100 bps hike, but markets appear to have taken Powell’s comments as fairly dovish. Perhaps this might be some wishful thinking, a la a small kid getting a maybe from a parent and taking it as a yes, and the comments didn’t quite sound the all-clear, reiterating that “we think policy is going to need to be restrictive”. What’s more policy-sensitive markets may be remiss in putting the umbrellas away if Powell’s other comment that “there’s probably some additional tightening, significant additional tightening in the pipeline” proves true.

“From farming to fizzy drinks”

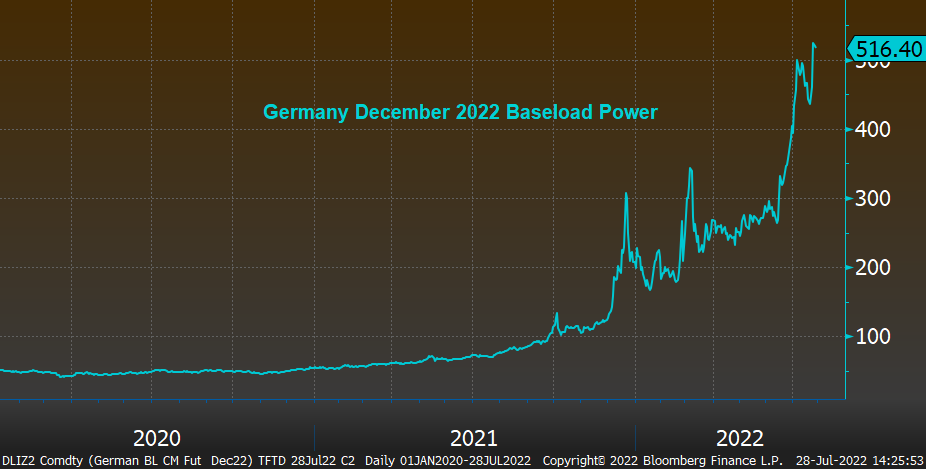

Another week, another round of energy headlines. While the usual pattern of increased prices continues amid muted flows from Russia, energy ripple effects continue growing in size and intensity. As this article from energy go-to Javier Blas explains, about a week ago, parts of London narrowly avoided a blackout by paying a record amount per megawatt hour, “more than 5,000% higher than the typical price”, “to persuade Belgium to crank up ageing electricity plants to send energy across the English Channel”. Power grid problems are also putting paid to development in parts of London as sufficient electrical capacity was not available until 2035. On the natural gas front, high prices are continuing to take a toll. BASF announced that it “is cutting ammonia production further due to soaring natural gas prices”, “with potential ramifications from farming to fizzy drinks” thanks to its role in the manufacturing of fertilizers and its production of carbon dioxide as a byproduct (déjà vu!). This will certainly not be welcome news for supply chains that are still reeling, with even vital supplies such as medicines running short in places such as France and Australia.

“Not an official definition”

The latest GDP print coming in on the wrong side of zero means that the US has now had two negative quarters in a row, and with it has come headlines trying to pin down what exactly the definition of a recession “is” (the Wikipedia page was locked at the time of writing and Powell offered that “it’s a broad-based decline across many industries that sustain for more than a couple of months and there are a bunch of specific tests in it”). Meanwhile, the Biden administration has been quick to push back on any suggestion that the US is in, or heading into, the dreaded economic r-word. While their assessment on jobs was broadly repeated by Powell, that is that “labor demand is very strong”, they risk inducing some degree of Streisand effect or maybe… Never believe anything until it’s officially denied?